Features Dienstwohnung als Sachbezug

Official residence as a benefit in kindA calculation tool for assessing the benefit in kind for company housing in AustriaBasicsA prosperous company leaves certain advantages to its employees, whether it is in the form of a company car or free or discounted living space or other.

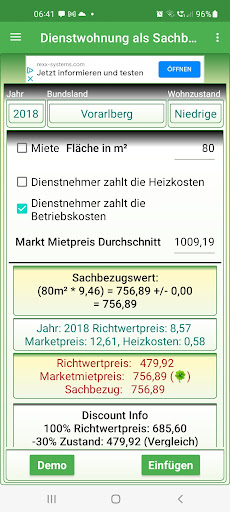

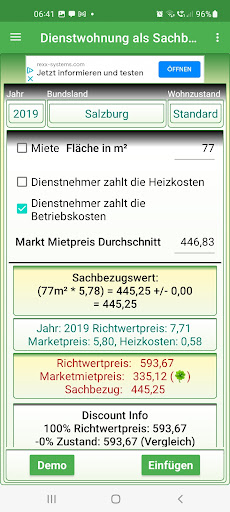

However, these advantages are monetary, so they are part of the monthly salary and increase the salary by this value and are taken into account for the duties, contributions and taxes.Assessment of the benefit in kindFor the assessment, official non-cash reference values are set by the Federal Ministry of Finance and, if not set, then the middle prices of the consumer location are to be made.Evaluation of the official residenceStatutory square meter values are specified in the Guideline Value Act and are updated annually.

The law prescribes how these values are used and which discounts or surcharges are to be calculated.

A procedure is also prescribed to achieve the best possible evaluation.Reductions from the guide value are as follows:• Apartment does not meet the standards (no heating or toilet) then 30%• Apartment for porter 35%• Employee pays the operating costs himself 25%SurchargesIf the heating costs cannot be determined based on actual values• Heating costs per square meter € 0.58 per month.The procedureComparisons are to be made between the benchmark value according to the law and the average price of the consumer location, the average price of the consumer location minus 25% compared to the benchmark value, first minus discounts then, to 50% then to 200% and as a result you have either the average price or the guide value as a value in kind plus the +/- heating costs.example100 sqm official apartment in Vienna as a consumer, sqm average price is € 12.97 The benchmark law from 2021 is € 5.80 and no discounts, how do you value?• Comparison (1) 50% guide value versus 75% mean price (-25%) -> € 2.90 versus € 9.72• Comparison (2) 200% guide value versus 75% mean price (-25%) -> € 11.60 versus € 9.72• For 1 and 2 you take the minimum, which results in € 2.90 against € 9.72, then you take the maximum of these, therefore € 9.72 * the square meter of 100 results in € 972.00 as material value.• If the employee does not pay the heating costs himself, add a surcharge of 100 * 0.58• If the employee pays the heating costs himself, the benefit in kind is reduced with these costs.• The result would then be € 972.00 + € 58.00 = € 1030.00 or € 972.00 - (€ 58.00?) = € 914.00

Learning Tools

Enhance your learning experience with interactive features.

Financial Tools

Manage your finances and track your expenses easily.

Food & Dining

Discover recipes and order food from your favorite restaurants.

See the Dienstwohnung als Sachbezug in Action

Get the App Today

Available for Android 8.0 and above